Frequently Asked Questions

Q - What are the system requirements for The Retirement Planner?

A - Windows 2000 or later and Excel 2000 or later. An Internet connection is required during installation and every few days to confirm that your license is up-to-date. A large, wide screen monitor is recommended, but not required.

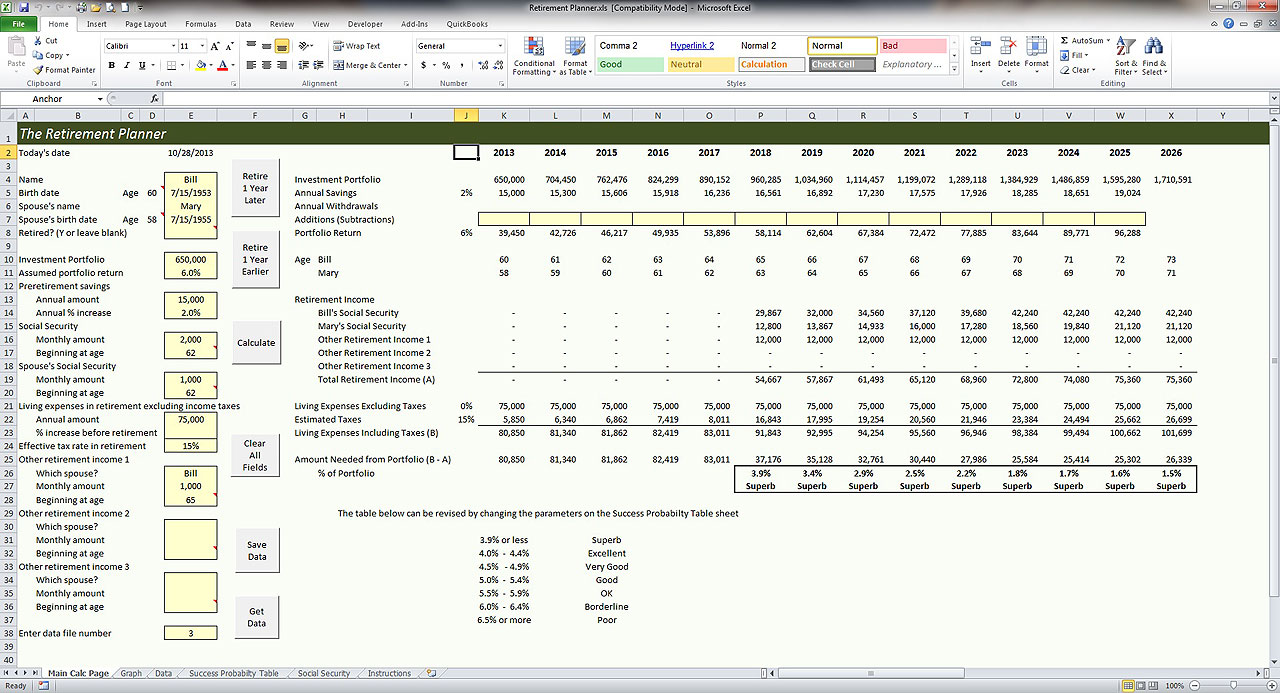

Q - Why isn’t the client’s employment income earned before retirement a data entry item on The Retirement Planner?

A - What matters is how much the client is saving each year, not how much they are earning. If a client earns $1,000,000 a year, but spends it all, that doesn’t get them any closer to a safe retirement.

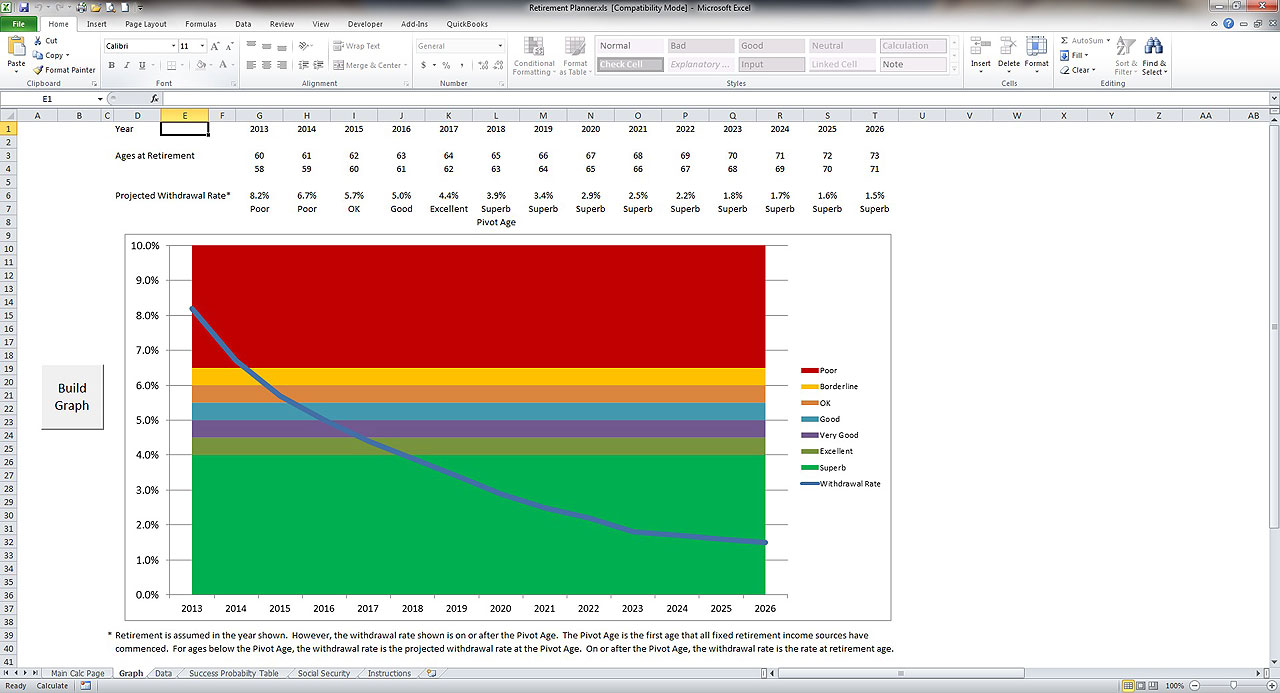

Q - Why does the portfolio withdrawal rate appear at the bottom of some columns, but not others?

A - The portfolio withdrawal rate only appears on or after the Pivot Age. The Pivot Age is the first age that all of the client’s lifetime retirement income (i.e., Social Security and defined benefit lifetime pensions) has commenced or will commence. Once all the client’s retirement income sources have commenced, the portfolio withdrawal rate represents a long-term rate that the portfolio will need to sustain for 30 or 40 years. This metric can be compared with benchmarks in literally hundreds of articles that have been published in the financial media regarding safe withdrawal rates. The portfolio withdrawal rate before the Pivot Age is a temporary rate and cannot be used as a metric in this manner.

![]()

|

|

| Click on screenshots to enlarge | |

|

|

*The Retirement Planner is only $99.00 first year with

$49.00 annual renewals